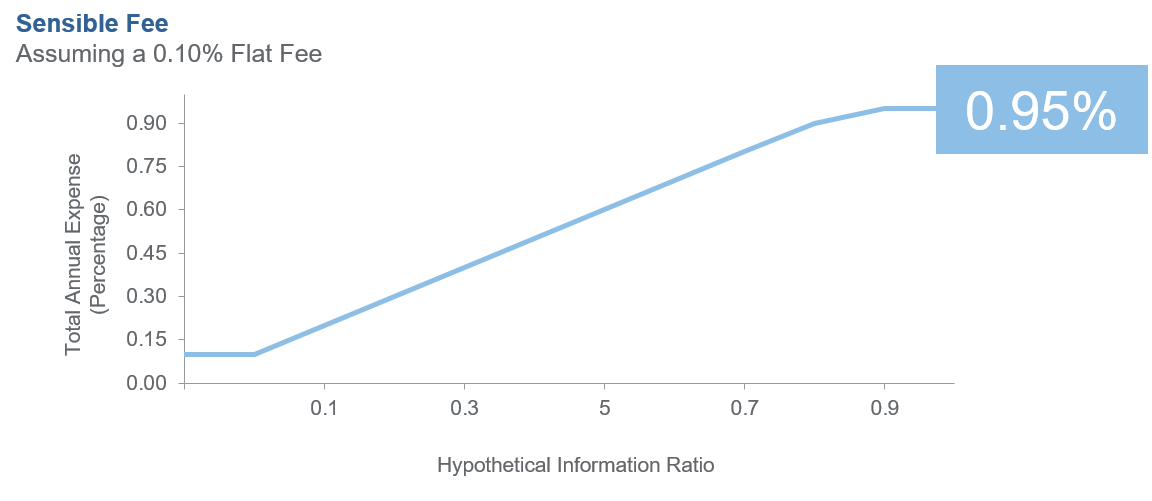

[ Base Fee + (IR X 100) ]

An industry first, WW IR Sensible Fees™ solve the fee problem by creating a simple structure with a pure zero or transparent low base fee for beta exposure plus a linear fee, directly linked to risk-adjusted outperformance only when it is earned, by using information ratio (IR).

IR is a measurement of excess return and the active risk taken relative to a specific benchmark. A positive IR indicates that positive excess returns were achieved over the measurement period while also taken into account the level of active risk used to beat the benchmark.

Westwood (WW) has developed a new, innovative and simple fee framework available to eligible investors on strategies or products in which we are offering an Information Ratio-Based Sensible Fee™ framework. This framework, called Westwood Sensible Fees™, embraces the core principles of evaluating pure manager skill, addressing the low cost of indexing and protecting investors using risk-based fees — all with the goal of changing the probability of winning in an efficient asset class and reversing the historical precedent set in the industry by giving the asset owner the asymmetric advantage.

A performance-based fee generally introduces the following risks: (i) Performance-based fee arrangements may cause Westwood to make investments that are more risky or speculative than otherwise; (ii) Westwood may receive increased compensation (compared to a fixed fee) based on unrealized appreciation as well as realized gains on assets in the client’s account, (iii) clients may pay a performance fee even if an account declines in value, and (iv) no compensation or refund is paid if Westwood underperforms the benchmark. Sensible Fees are only available to those investors which are \”qualified clients,\” as defined in Rule 205-3 of the Investment Advisers Act of 1940.

Notifications