Technology is still strong, driving the S&P to new highs. It’s interesting to note that despite the technology sector’s continued strength, the mode has been through higher expected earnings — the forward price to earnings multiple has either decreased or remained flat. Not so this quarter. The strength came from “multiple expansion” — the market crowd reports that the trend of technological innovation driving margin expansion and higher revenue growth is going to continue.

Following are the main takeaways from this quarter’s market review. If you have any questions, please reach out to your advisor.

- The S&P 500 and Nasdaq closed the quarter at new highs, with the S&P 500 marking its 32nd record close of the year and the Nasdaq its 21st.

- Information technology was the best-performing sector, gaining 14.5% in the quarter.

- Inflation showed some signs of easing, with the personal consumption expenditures (PCE) price index for May rising at its slowest pace since March 2021.

- The Federal Reserve kept interest rates at current levels during its May and June meetings, keeping a cautious stance on potential rate cuts.

- First-quarter GDP growth was reported at 1.4%, a deceleration from the fourth quarter’s 3.4% growth.

- The unemployment rate increased slightly to 4.0% in May, with 272,000 new jobs added.

- Consumer confidence dipped in June to 100.4, down from 101.3 in May, according to the Conference Board Consumer Confidence Index®.

- Gold prices reached a record high of $2,450 per ounce in May, driven by anticipated interest rate cuts and increased demand from Asian central banks.

- The housing market showed mixed results, with existing home sales falling but new home prices reaching new highs.

- International markets had varied performances, with the UK showing signs of economic recovery, while China faced challenges in its retail and industrial sectors.

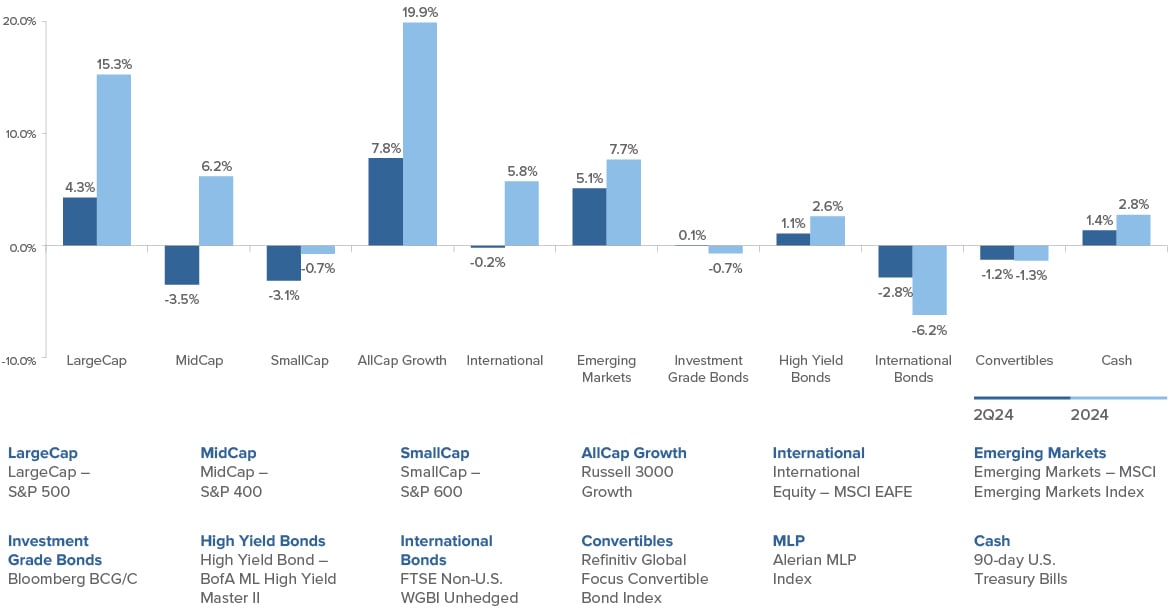

Market Snapshot | Asset Class Performance