Todd Williams, CFA®

Todd Williams, CFA®

Price Dislocation Creates Investment Opportunity With Large-Cap Insurer

The Westwood U.S. Value team believes that investing in undervalued, high-quality businesses can generate a return premium, resulting in lower absolute downside risk and superior risk-adjusted returns. The team uses fundamental analysis to identify high-quality businesses that exhibit strong return on invested capital, low leverage, disciplined capital allocation and resilient, consistent growth. They seek stocks trading at a discount to their peers, the industry or the market. And they invest in “best ideas” to capture the return premium from stocks trading at the intersection of quality and value, resulting in portfolios designed to outperform over the long term.

Introduction

Progressive Corp. (PGR) has underperformed the overall equity market and the broader financial sector in 2025. We believe this is primarily due to two main factors:

-

Market Sentiment

Property & casualty insurance has not been a preferred industry in a market that has prioritized themes such as high growth, high beta and anything related to artificial intelligence. Specifically, auto insurance has a value tilt, is one of the higher-quality financial subsectors given the visibility of earnings, and typically has lower volatility than the overall market.

-

Decelerating Growth

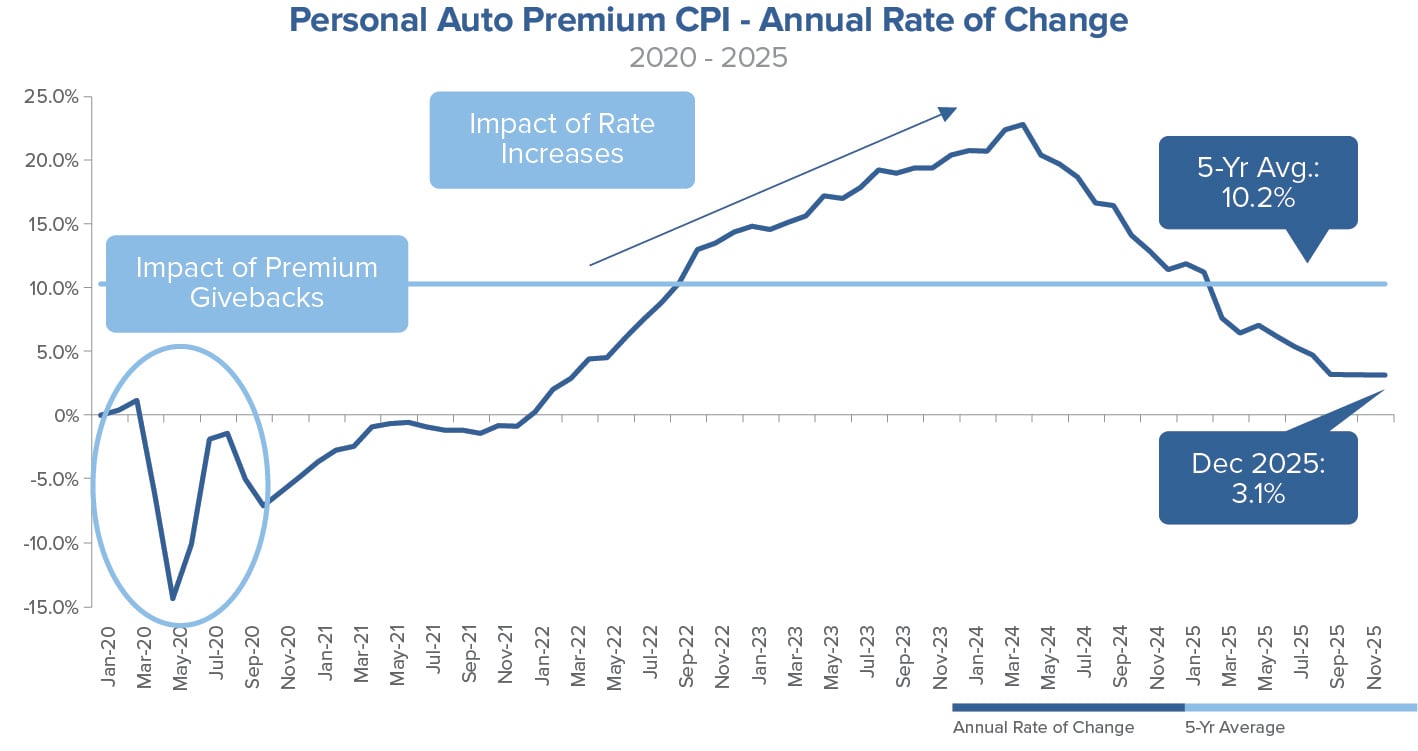

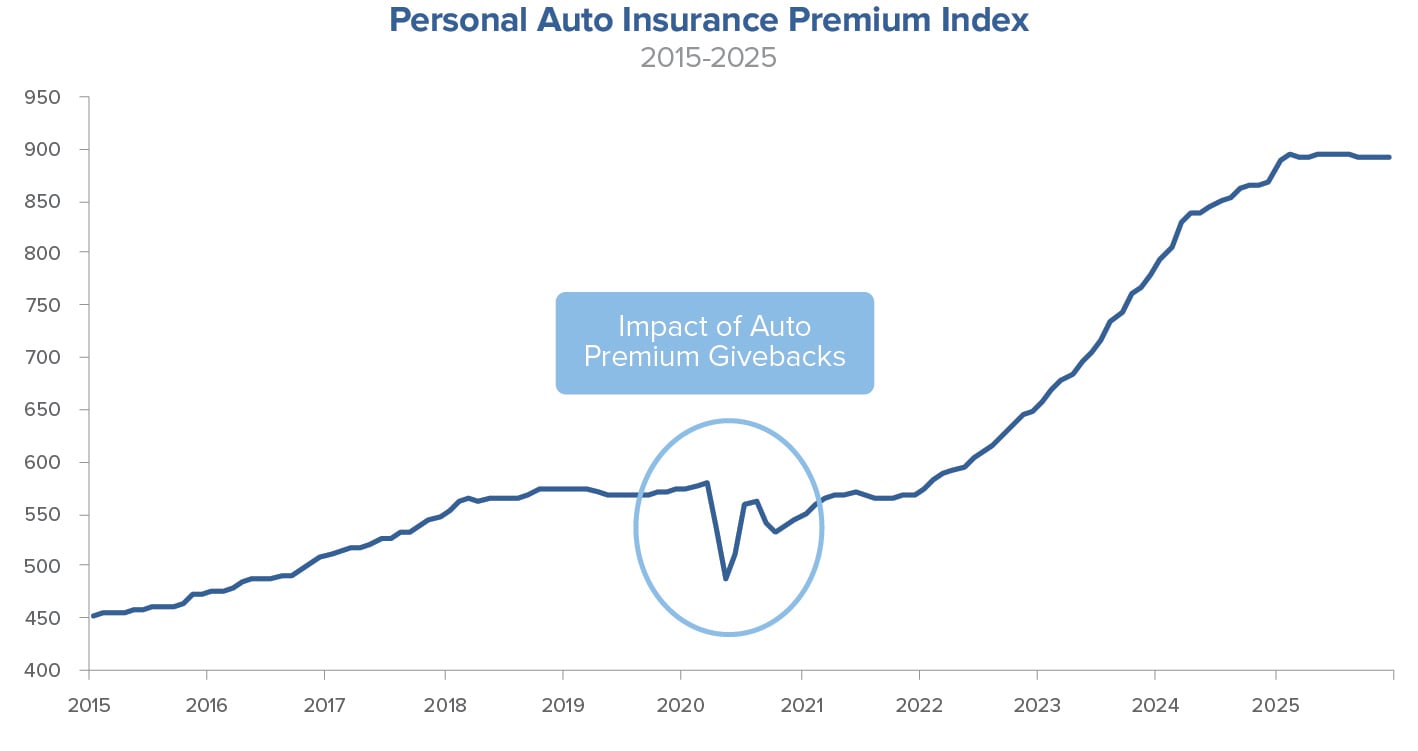

The industry is getting more competitive, as evidenced by company commentary and lower insurance rate increases. A sign of growing competition in the marketplace is the continued shopping trend among auto insurance shopping consumers. These trends may lead to a slowdown in premium growth and potentially pressure profit margins, which are at record levels. One oft-cited data set is the deceleration in auto premium growth as measured by the BLS.

Investment Opportunity

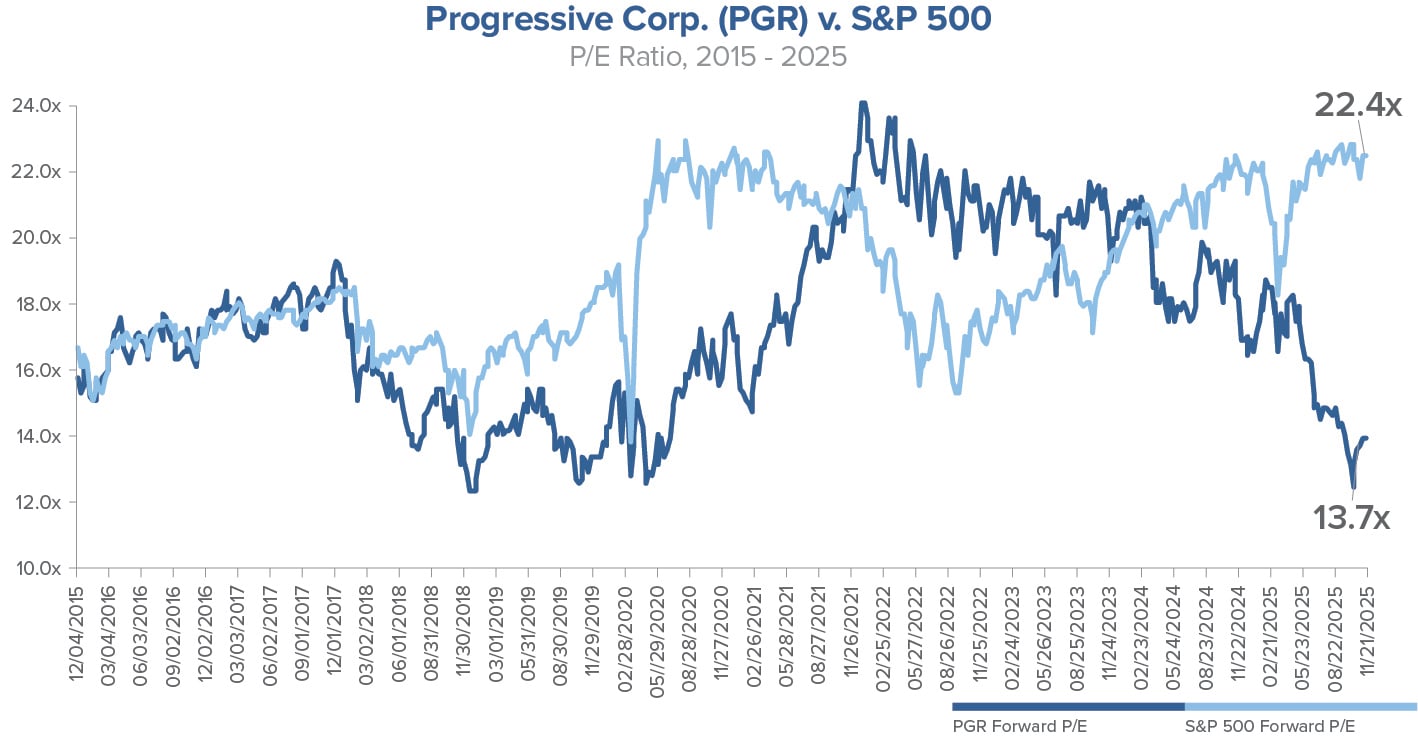

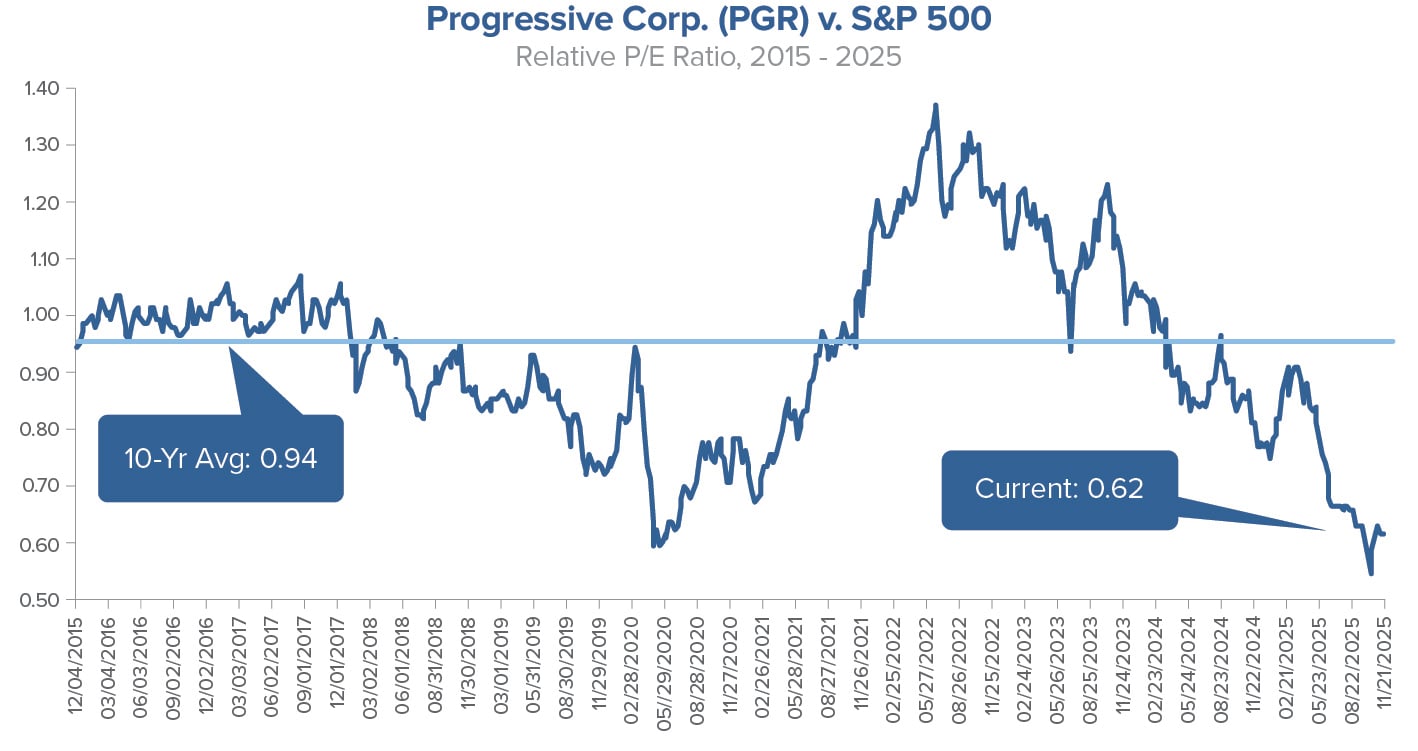

As long-term investors, we have the ability to use a long-term time horizon to our advantage. Progressive has a long track record of outperforming the competition and delivering excellent shareholder returns. Today, we believe the company is in the strongest market position in its history, yet the valuation is near a historic low, both in absolute and relative terms to the S&P 500.

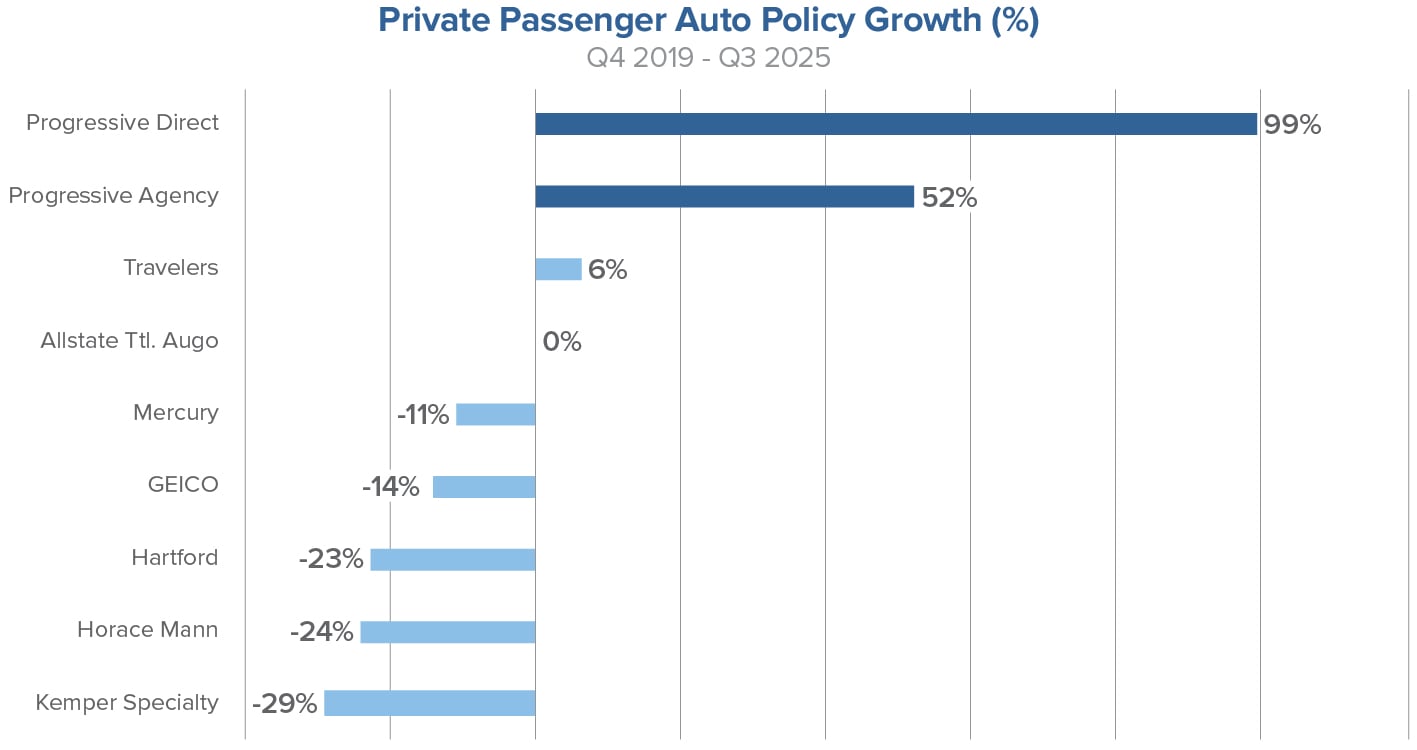

A slowdown in policy growth and lower profit margins is already expected and built into forward consensus estimates. The industry is coming off a period of unprecedented growth and profitability that was never expected to continue indefinitely. Although Progressive’s policy growth has slowed from +21% to +12% annually, this is in the context of an auto insurance market that grows 1-2% per year, with large peers growing 0-2%.

Progressive has gained significant market share from this policy growth profile. This is important, not only from a competitive view, but more importantly from a scale standpoint. Auto insurance is a scale business, thus, a larger customer base results in better operating leverage in future periods, which should lead to higher earnings potential.

In calendar year 2025, the company was expected to grow earnings per share (EPS) by 26%, and tangible book value per share has grown 39%. Furthermore, earnings estimate revisions have been materially positive for both calendar years 2025 and 2026. With the company’s valuation near trough levels, we believe any concerns over slowing price increases are already priced into shares.

Conclusion

When we invest in a stock, we consider ourselves owners. And as owners of a business, we want sustainable, profitable growth that compounds over time. In the insurance business, compounding occurs because good management teams strategically accelerate policy growth when profitability warrants and slow topline growth when industry conditions become more competitive. Progressive’s management team is executing the discipline we expect in a challenging environment: avoiding unprofitable policy growth during a period of elevated competition and leveraging scale, brand strength and technological advantages to capture market share when the profit cycle supports it.

When the market rotates away from the most volatile, richly valued areas of the market that are currently in favor, we expect shares of Progressive to benefit due to the compelling reward-to-risk at current levels.