Adrian Helfert

Adrian Helfert

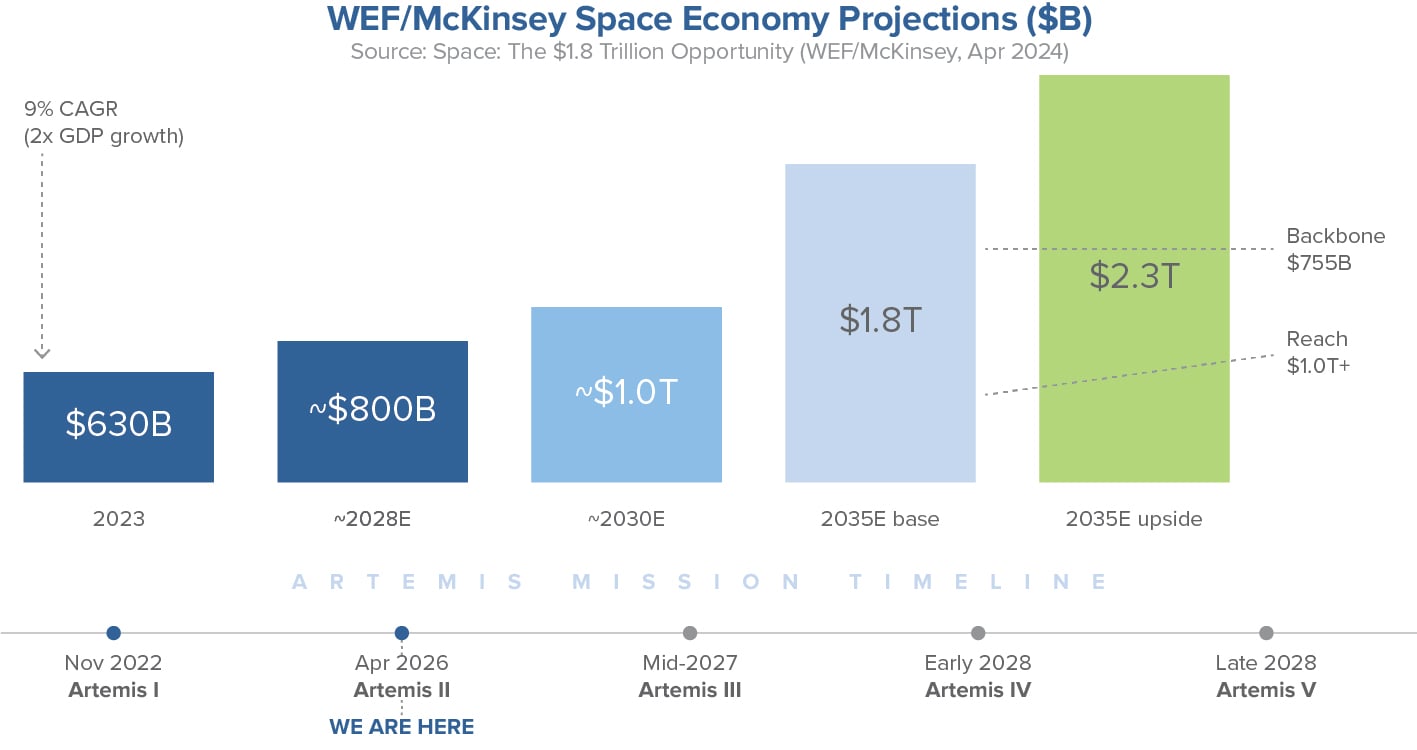

On April 10, 2026, NASA’s Artemis II crew splashed down in the Pacific after a 10-day, 694,481-mile lunar flyby — the first crewed mission beyond low Earth orbit in over 50 years. I watched in a pub on an iPad with similarly interested friends while the vast majority of people didn’t know it was happening and certainly weren’t feeling the sense of importance of this mission success. The mission validated the Orion spacecraft’s life-support and deep-space navigation systems, setting a new human spaceflight distance record of 252,756 miles from Earth. This was not merely a symbolic milestone. It was a technical proof-of-concept that unlocks a multi-decade investment cycle in lunar infrastructure, commercial space services and national defense. According to the World Economic Forum and McKinsey & Company, the global space economy is projected to grow from $630 billion (2023) to $1.8 trillion by 2035 — a 9% compound annual growth rate that is roughly twice the projected rate of global GDP growth and comparable to the semiconductor industry’s trajectory. In an upside scenario driven by improved data access and reduced launch costs, the figure could reach $2.3 trillion. We believe Artemis II accelerates this timeline by de-risking the Orion platform and signaling sustained U.S. commitment to deep-space operations.

What Artemis II Proved

Artemis II was the first crewed flight of both the Space Launch System (SLS) rocket and the Orion spacecraft. The crew — Commander Reid Wiseman, Pilot Victor Glover, and Mission Specialists Christina Koch and Jeremy Hansen (CSA) — tested Orion’s life-support systems, performed manual piloting demonstrations, evaluated emergency procedures and conducted scientific investigations, including human tissue response to deep-space radiation. Critically, the crew took manual control of the spacecraft to validate handling characteristics that will inform future rendezvous and docking operations with commercially built lunar landers. The mission confirmed that Orion can sustain humans in deep space, clearing the path for surface missions. NASA has stated that focus now turns to assembling Artemis III and preparing for the first crewed lunar landing since 1972.

Artemis Mission Roadmap

The following timeline outlines NASA’s planned cadence, which is designed to build toward a permanent lunar presence and eventual Mars missions:

| Mission | Target | Objective and Investment Significance |

| Artemis I | Nov 2022 | Uncrewed test flight. Validated SLS and Orion systems. Completed. |

| Artemis II | Apr 2026 | Crewed lunar flyby. Validated life support and deep-space ops. Completed. |

| Artemis III | Mid-2027 | Crewed Earth-orbit test of SpaceX Starship HLS and/or Blue Origin Blue Moon landers. Critical for lander certification. |

| Artemis IV | Early 2028 | First crewed lunar landing since 1972. Two astronauts to lunar South Pole. Triggers surface infrastructure spending. |

| Artemis V | Late 2028 | Second landing; begins construction of permanent Moon base. Sustained demand for habitation, power and ISRU systems. |

| Artemis VI+ | 2029+ | Annual lunar landings. Commercial partnerships scale. Mars architecture development begins. |

The Space Investment Landscape

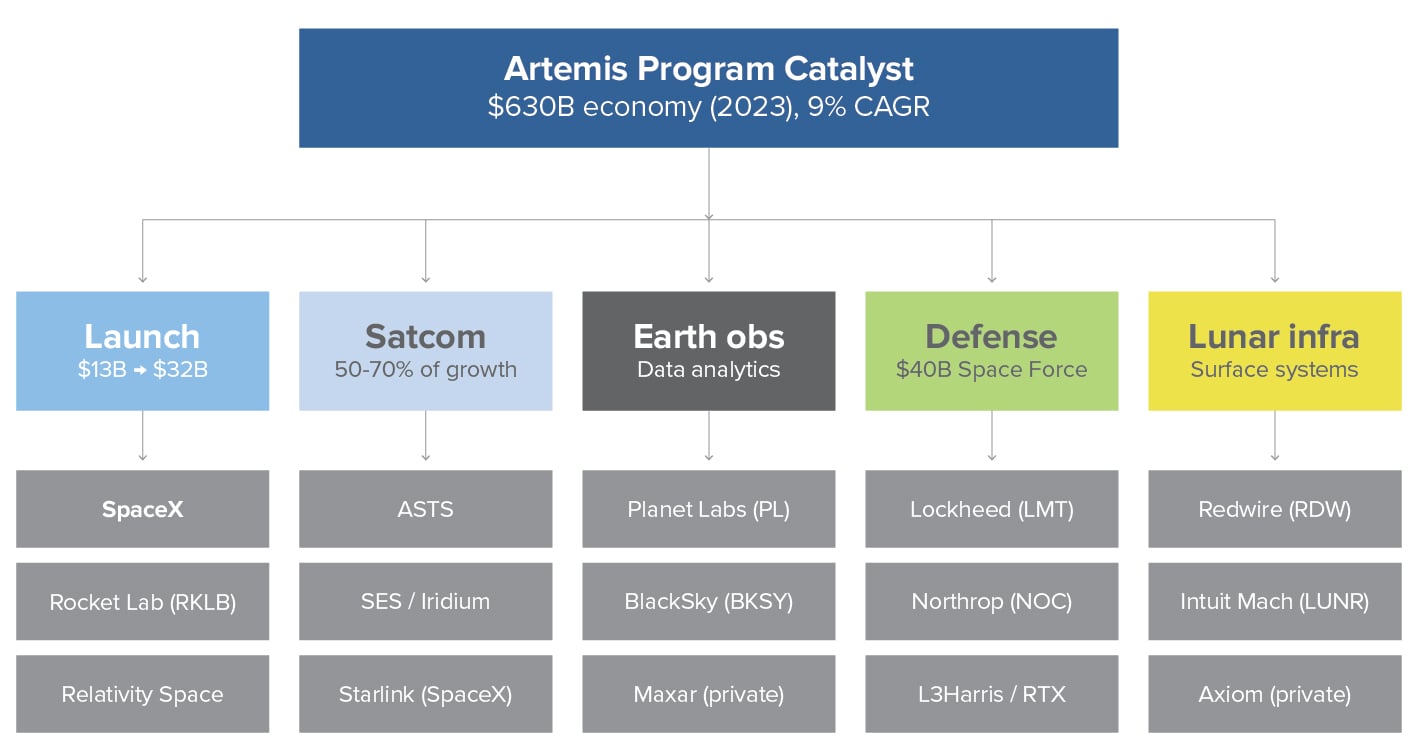

The commercial sector accounts for 78% of the global space economy and employs nearly 400,000 people in the U.S. alone. The WEF/McKinsey framework divides the space economy into two segments: “backbone” applications (satellite manufacturing, launch, ground operations — $330 billion in 2023, growing to $755 billion by 2035) and “reach” applications (industries that depend on space-enabled data and services — $300 billion in 2023, growing to over $1 trillion by 2035). Five sectors — supply chain and transport, food and beverage, defense, retail and consumer, and digital communications — are forecast to generate 60% of the space economy by 2035. Reusable rocket technology has reduced launch costs by roughly 10x over the past two decades, the launch sector alone is projected to grow from $13 billion to $32 billion by 2035, and satellite launches have grown at a 50% annual rate. The Trump administration has allocated $40 billion to Space Force for orbital defense, and NASA has deliberately structured Artemis work as commercial contracts — creating recurring revenue streams for private-sector partners. A potential SpaceX IPO, reported at a valuation of up to $1.75 trillion, could catalyze a broader re-rating of the entire space sector.

We organize the opportunity set into five investable themes:

- Launch Services and Reusable Rockets: SpaceX (private; IPO anticipated June 2026), Rocket Lab (RKLB), Relativity Space (private). Declining launch costs drive volume growth across all downstream segments. The medium-lift race — Neutron, Terran R, New Glenn — will produce two to three winners by 2028.

- Satellite Communications and Connectivity: AST SpaceMobile (ASTS), SES, Iridium. Satellite broadband represents up to 50-70% of projected space economy growth (Morgan Stanley). Direct-to-device connectivity is the next frontier.

- Earth Observation and Data Analytics: Planet Labs (PL), BlackSky Technology (BKSY), Maxar (private/acquired). Defense and intelligence demand drives recurring revenue; Gen-3 satellite constellations deliver sub-meter resolution imagery.

- Defense Primes and Space Security: Lockheed Martin (LMT), Northrop Grumman (NOC), L3Harris (LHX), RTX, Kratos (KTOS). The $40B Space Force allocation and Golden Dome program ensure sustained demand. Lockheed builds the Orion spacecraft; Northrop supplies SLS boosters and is building habitation modules.

- Lunar and Orbital Infrastructure: Redwire Space (RDW), Intuitive Machines (LUNR), Axiom Space (private), SpaceX HLS, Blue Origin (private). As Artemis moves to surface missions, demand for landers, habitation modules, power systems and in-situ resource utilization (ISRU) will accelerate. NASA has structured these as commercial contracts with recurring award cycles.

For diversified exposure, the Procure Space ETF (UFO) and Tema Space Innovators ETF (NASA) offer broad space-economy exposure. UFO has outperformed the S&P 500 with 17.4% YTD gains through March. The NASA ETF includes pre-IPO SpaceX exposure — a notable differentiator.

Outlook: From Exploration to Infrastructure

The WEF/McKinsey report draws an explicit comparison: The space economy’s trajectory mirrors that of semiconductors, which grew from $600 billion in 2021 at 6-8% annually and are now foundational infrastructure. Space is following the same arc. Artemis II’s success confirms that the engineering works. What follows — lunar landers tested in 2027, boots on the Moon in 2028, a permanent base by 2029 and annual landings thereafter — will generate sustained demand across launch, communications, materials, habitation and defense. The ISS is scheduled for deorbit by 2030, creating a multi-billion dollar commercial space station replacement market (Voyager’s Starlab, Vast’s Haven-1, Axiom modules). Orbital data centers are emerging as a real concept. And Mars remains the stated long-term objective. Critically, the WEF/McKinsey analysis shows that “reach” applications — industries that depend on space data but are not themselves space companies — will account for more than half of the 2035 economy. This means the investment opportunity extends well beyond aerospace names into agriculture, logistics, insurance, autonomous vehicles and digital communications. For institutional allocators, the key insight is that space is transitioning from an exploration program to a capital expenditure cycle. The companies building this infrastructure today — whether through launch services, satellite constellations, defense contracts or lunar surface systems — are positioned for a multi-decade growth runway. Investors should build exposure now, calibrated to risk tolerance, while the sector is still early and the market is still pricing in uncertainty.