Jordan Latimer, CFA®

Jordan Latimer, CFA®

This year has ushered in a new phase of the AI investment cycle, creating a distinctive impact on both the markets and economy. During the second half of 2025, foundation models showed significant improvements and gave rise to agentic systems — a new class of technology capable of carrying out complex multi-step reasoning and technical processes. These highly capable systems are increasing disruption risk and creating new market opportunities. A generational technology shift is crowning new winners and calling into question the durability of historically “wide-moat” businesses.

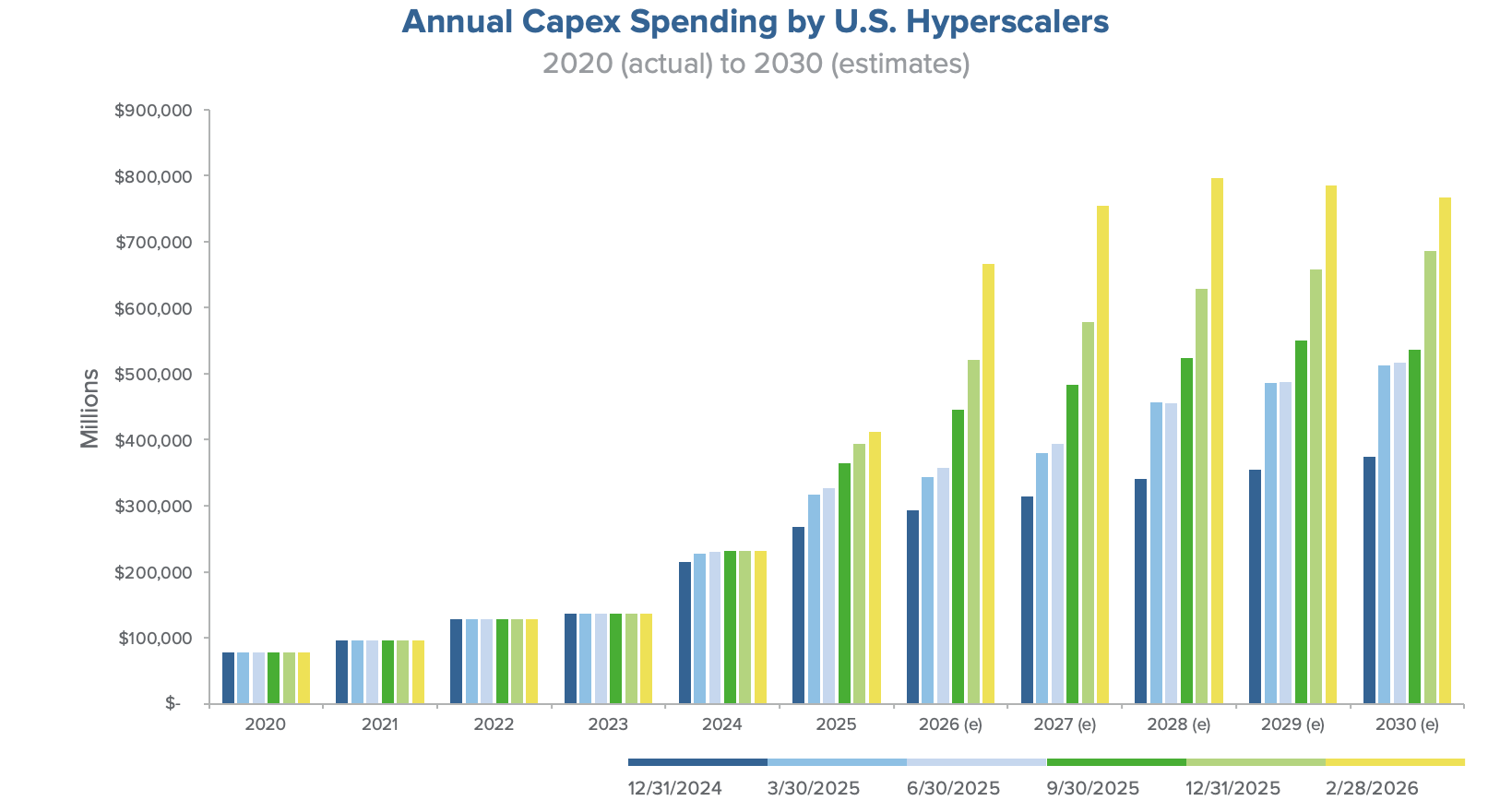

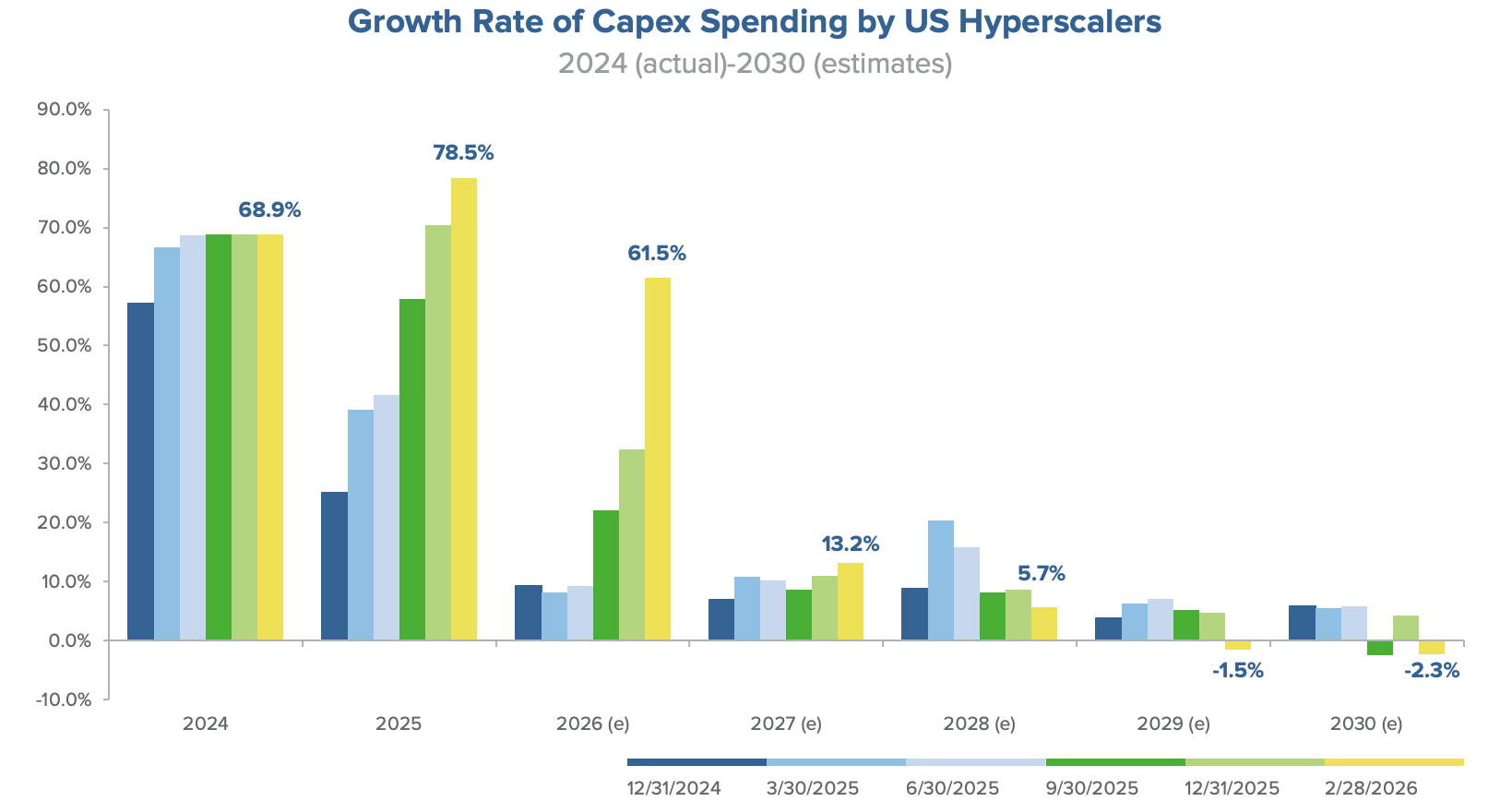

Growth Trajectory of Capital Expenditures Slowing

To support the massive demand for AI training and inference workloads, AI capital expenditures (capex) expectations have accelerated meaningfully year to date. Alongside the fourth quarter results, several U.S. hyperscalers — five U.S. based companies that have sprinted to the forefront of artificial intelligence capabilities — raised capex guidance to start the year. In the first two months of 2026, expectations for the top U.S. hyperscalers have already been revised upward by 30% to over $650 billion. Notably, expectations for 2026 capex have more than doubled since the beginning of 2025.

While markets are discounting a higher rate of spending, they are increasingly skeptical about the persistence of its growth. Although capex in absolute terms has been revised higher, the increase in expectations for the out years of 2029-2030 has been proportionally lower than for 2026-2028. This means that the second derivative of capex spending through 2029-2030, the growth rate, has declined and recently turned negative for the first time in 18 months. In the near term, we expect the ability of hyperscalers to show upside to growth expectations in the coming quarters to be a key driver of AI capex revisions.

Due to the capital-intensive nature of these investments, Returns on Invested Capital (ROIC) are expected to decline across the sector, placing downward pressure on valuation multiples. Longer term, hyperscalers must prove they can capture value from heavy infrastructure investment to drive ROIC to historical levels. Investors will be watching for how hyperscalers can drive both growth and importantly, ROIC from these significant investments.

Hyperscalers Turn to Debt for Capex Plans

Another change is that the source of funds for AI capex have shifted from primarily free cash flow (FCF) to, increasingly, debt and off-balance sheet financing arrangements. For example, Oracle recently issued a combination of debt and mandatory convertibles while signaling potential equity issuance to fund their capex plans. Additionally, Google, Meta, Amazon, and Microsoft have issued between $20 and $40 billion in debt for capex. In aggregate, U.S. hyperscalers are projected to issue approximately $150 billion in new debt in 2026, which has been well-received in the marketplace.

The $650 billion in capex represents roughly 90% of aggregate cash from operations (CFO) – the highest investment intensity to date. However, because cumulative CFO for these firms has grown over 25% annually since 2023, they remain within their cash flow limits and maintain ample debt capacity. Nonetheless, reliance on debt makes the AI cycle more credit-dependent and prone to deterioration in credit conditions, which could slow capex and, by extension, impact economic growth.

AI is creating significant macroeconomic cross currents at a crucial time for the U.S. economy. Massive data center construction has driven industrial activity and concentrated excess returns within the semiconductor industry. Accelerating demand has now pushed supply chains to full capacity. Skyrocketing prices for memory and storage have triggered cost inflation and demand destruction in other sectors. Energy scarcity has emerged as a major bottleneck, forcing developers to use “behind-the-meter” power sources, which may lead to further infrastructure delays.

Critically, the speed at which AI unlocks productivity gains will be key to offsetting inflationary pressures. While 2025 unlocked agentic capabilities, 2026 may be the point where these fundamental changes begin to cascade across the U.S. economy. Having the resources and experience to identify these opportunities is critical to capitalizing on emerging technology-driven investment themes.