On December 22, 2017, President Trump signed into law “The Tax Cuts and Jobs Act,” a sweeping 500-page tax reform for both individuals and businesses alike. This is the largest tax reform in three decades. The business tax reform is aimed at stimulating U.S. economic development while the individual tax reform provides a small degree of tax simplification with some short-term tax relief for most families.

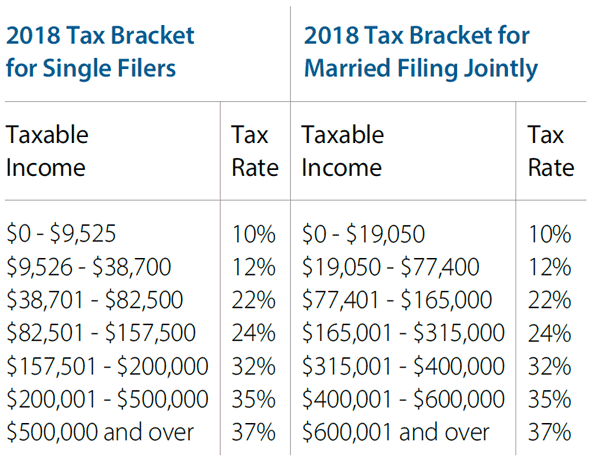

The number of federal income tax brackets for individuals is maintained at seven; however, the tax rate declines for taxpayers above the 10 percent tax bracket.

A key aspect of the tax reform was the consolidation and expansion of the standard deduction and personal exemption into a single larger deduction. The amount for personal exemptions is reduced to zero, and the standard deduction is nearly doubled to $12,000 for single filers and $24,000 for joint filers. The additional benefit of the standard deductions for the elderly and blind are retained.

Many previous itemized deductions have been eliminated or reduced.

- The deductions for state and local tax (SALT) is limited to $10,000 annually for any combination of state and local property taxes or sales taxes.

- The mortgage interest deductions are limited to interest on the first $750,000 of acquisition debt originating after 2017.

- Additionally, the interest deduction for home equity loans or home equity lines of credit is no longer allowed. Existing loans will not be grandfathered.

- Miscellaneous itemized deductions are eliminated for unreimbursed employee business expenses, investment expenses, tax planning expenses or expenses allowed under the hobby loss rule.

- The threshold for deducting medical expenses is reduced to 7.5 percent of adjusted gross income (AGI) for 2017 and 2018. After 2018, the medical expense deduction reverts to the 10 percent of AGI threshold.

- Cash gifts to public charities are deductible as long as the gift does not exceed 60 percent of the taxpayer’s adjusted gross income. Contribution amounts exceeding the 60 percent limitation can be carried forward by the taxpayer and deducted for up to five years.

- Deductions for casualty and theft losses are eliminated with the exception of losses incurred in federal disaster areas.

- Itemized deductions are no longer limited based upon income limitations.

The alternative minimum tax (AMT) system is retained for individuals, but the exemptions amount and the thresholds for phasing out exemptions are significantly increased. As a result, the AMT exposure should be much less, given the limited itemized deductions.

The child tax credit is increased from $1,000 to $2,000 for children under age 17. This tax credit begins to phase out for taxpayers with income over $400,000

(married filing jointly) or $200,000 (single). A non-child dependent credit of $500 per person will also go into effect for dependents age 17 and older, including

the elderly.

Moving expenses related to a job change can no longer be deducted unless you are in active military service.

The penalty for an individual failing to maintain minimum insurance coverage, as defined by the Affordable Care Act, will be repealed beginning in 2019.

For any divorce or separation agreement executed after December 31, 2018, alimony and separate maintenance payments are not deductible by the payor spouse and are not included in the income of the payee spouse. The tax rules for child support remain unchanged.

The tax on unearned income of a child, also known as “kiddie tax,” will now apply estate and trust tax rates to the net unearned income of a child. The child’s tax will no longer be affected by the tax situation of their parent.

Distributions from Section 529 plans have been expanded to include tuition expenses at public or private elementary schools and high schools. Annual distributions from 529 plans for these expenses are limited to $10,000 per child. The good news is, this tax provision in the new law is permanent and will not expire.

For estates and gifts made between 2018 and 2025, the act doubled the base estate and gift tax exemption amount from $5 million to $10 million per person. The exemption amount is indexed for inflation, with 2011 being the benchmark year, and is expected to be approximately $11.2 million for an individual in 2018.

The income tax bracket for trusts and estates is reduced to four brackets with 37 percent being the top rate set on taxable income over $12,500.

Finally, many of the tax brackets and limits are now indexed to a new measure of inflation called the Chained-Consumer Price Index for All Urban Consumers (C-CPI-U). The previous index was the Consumer Price Index for Urban Consumers (CPI-U). Over the long term, it is possible that C-CPI-U could act as a tax increase if income/wages grow faster than tax brackets and standard deductions benchmarked by C-CPI-U.

As with previous tax law changes, lawmakers could potentially adjust the current tax rules or make the rules permanent before many of these tax provisions sunset on December 31, 2025. We encourage you to meet with your tax advisor to discuss how these tax changes might impact you.

Westwood Trust and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for information purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.