If you asked most investors at the end of 2018 where the country would be at the conclusion of 2019, few would have guessed markets would be at record highs, our president impeached (not convicted), and the federal funds rate down at 1.625%, and moving lower, even as the American economy seems to have a renewed strength.

To be fair, the road that led to where we are today has been winding and the path ahead may meander and grow increasingly complicated as we enter an election year where uncertainties still surround an increasingly positive outlook. As we recap the past 12 months and look ahead to the first couple quarters of the new decade, we will do our best to ensure you have enough information to get a jump on 2020.

Markets, Interest Rates and Global Health

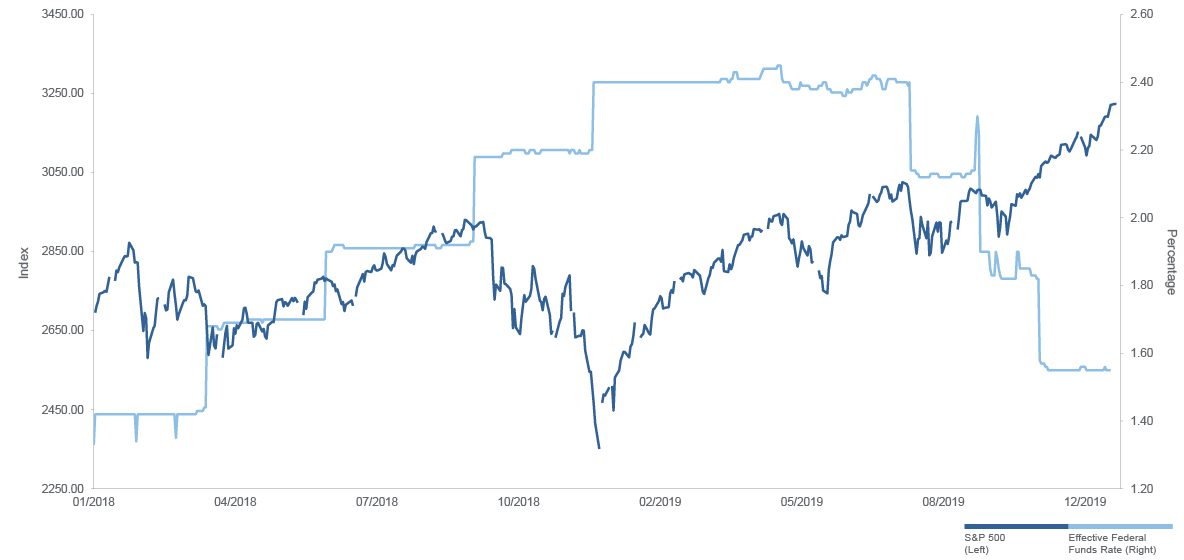

The U.S. economy carried on its record-breaking, 127-month-long expansion that continues to push domestic equities higher and higher. After the v-shaped recovery in stocks during the first half of 2019, driven mainly by the Federal Reserve’s abrupt reversal to a more accommodative interest rate policy, the impetus behind the back half’s performance has been motivated by rates and the culmination of several factors that have helped build confidence.

The current sentiment landscape remains cautiously optimistic as we pointed out in our mid-year review, but previous concerns of impending recession seem to be fading (at least momentarily). The current consensus of economists and analysts seem to be increasingly optimistic that recession is not only far off, but some believe that 2021 may bring increased GDP output compared to 2020. That said, most don’t see the President’s target of 3% growth being attained — and that’s OK.

The Federal Open Market Committee (FOMC) did find it appropriate to cut interest rates a total of three times during the year, taking the wind from the sails of safe harbor investments like savings accounts and redirecting them into more risky assets like stocks and even real estate. Both are currently at record levels and most believe there’s more upside to come.

The reality is that the tighter monetary policy of late 2018 was contrary to much of the globe’s interest rate position. It was almost inevitable that our modestly growing economy, in need of export dollars and consumer spending, could get a boost from lower cost of capital and a cheaper U.S. dollar. So far, it’s working as the U.S. trade deficit narrows and consumers’ spending continues to feed the economic machine.

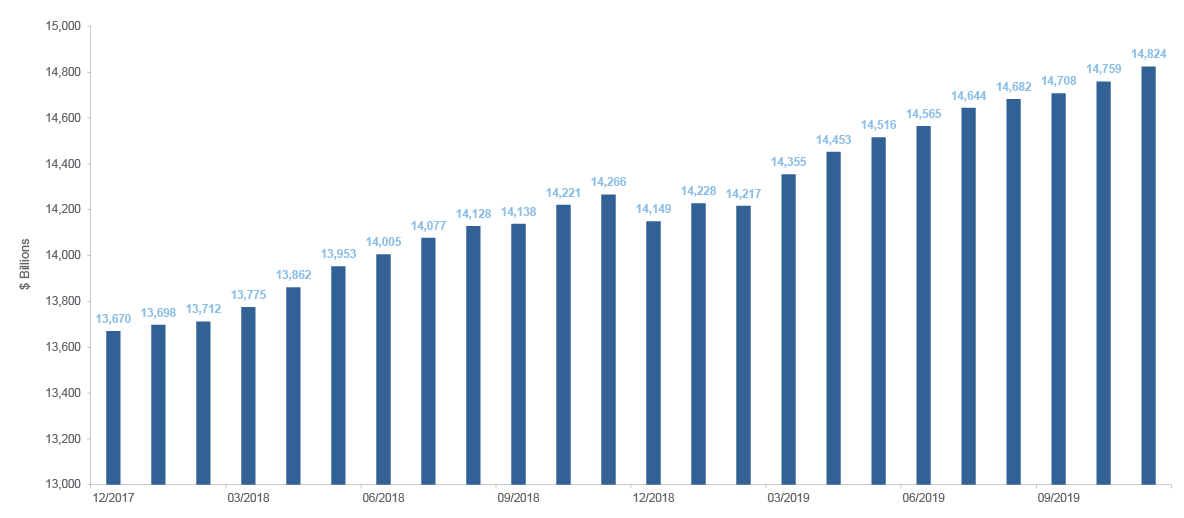

Personal Consumption Expenditures

Billions of Dollars

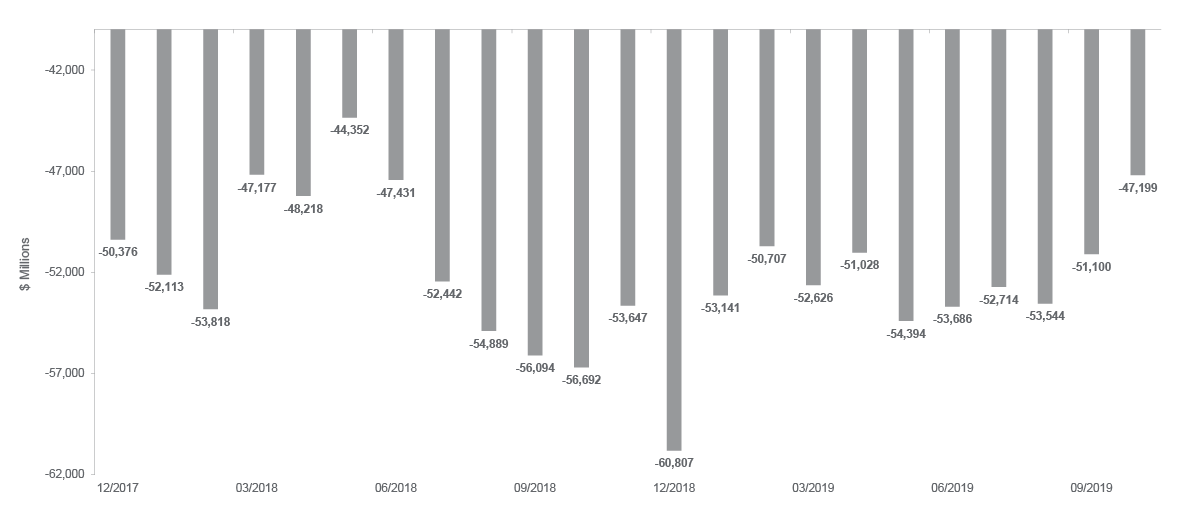

Trade Balance: Goods and Services

Millions of Dollars

There are several countries who’ve gone beyond a typical accommodative stance and entered into an almost irrational negative rate environment. Experts are still unclear of the long-term effects, but we know upside-down interest rate anomalies can heavily distort financial markets as consumers and businesses are almost forced to behave in unnatural ways. Some warn of the obvious systematic dangers to pensions and insurance funds; other warnings are far more ominous (if you can imagine).

A complete reversal of widely accepted money logic, where borrowers are paid to take on debt and safe haven investments’ returns are guaranteed negative are certainly offputting for even the most progressive thinker. For now, let’s assume these risks remain contained and isolated and monitor effects over time.

That said, interest rates across many areas of Europe are below 1%, fueling a potential housing bubble across the pond as institutions put their war chests of cash to work snapping up real estate at never-seen borrowing rates. Even with these extremely accommodative policies, the EU is expected to grow at just 1.4 to 1.6% in 2020 according to the European Commission — others have a less optimistic outlook. This is an area we will continue to monitor closely.

It is also unlikely that the FOMC will be as rate aggressive in 2020 as unemployment remains at near 50-year lows, the stock market at all-time highs, and our economy at least stable and maybe poised for one last hurrah. These factors will likely strengthen the probability of a rate floor for the first half of the year. In turn, mortgage rates aren’t likely to fall much further over the next six months, which should tempter the continued appreciation in the housing market.

Another tail risk that’s become less concerning is Brexit. After UK Prime Minister Boris Johnson’s conservative party won a parliamentary majority, members then went on to pass Johnson’s EU withdrawal agreement to the House of Lords where it will likely be debated this month, but should end in an EU exit by Jan. 31. Many believe that while the full outcome of Brexit is unknown, its passing could reinvigorate the UK’s economy, so long as trade deals are favorable. Many other nuances remain, but at least now the region has a firm direction to move in — this should be a net positive.

U.S. corporate earnings growth remains tepid, with 2020 S&P 500 consensus estimates dropping below $180. The late year (2019) rebound in energy prices may offer a modest boost as cheap crude prices created a profit drag. But it still seems growth is expected at a decent, but not elevated pace. And even though domestic valuation estimates are likely conservative, we continue to see strength in value- and defensive-oriented sectors in the first half of 2020. The breadth of market performance is also likely to be more limited as rising tides will lift fewer ships in this end-of-cycle encore.

Hope, the Consumer and Federal Spending All Contribute

Perhaps what’s most intriguing about the last quarter’s rally is that much of it seems to be based on hope. Hope that the initial U.S.-China trade deal (which is to be penned in January) blossoms into something much broader; hope that the new USMCA agreement, still yet to be ratified, boosts our economy; hope that President Trump’s impeachment and the media circus surrounding it and the coming election in general, doesn’t hinder our delicate expansion; and obviously, hope that corporate earnings turn a corner and reverse the slowing growth trends we’ve seen over the last few quarters.

There is some logic to this confidence, and it’s more than just coincidence that markets are rising. Data shows that American consumers are spending again — and we see this from several angles. The Household Savings Rate, while relatively stable since mid-2019, is a full percentage point lower than it was in December of last year, suggesting that there’s less fear gripping our wallets. Also, households are increasing their incomes a bit more than they are growing their spending, giving us that slow savings rate increase. From the spending side, digital and traditional holiday sales are expected to make new records in 2019, both up in the double digits over last year. The more conservative National Retail Federation sees overall holiday spending up 4% year over year as consumer confidence continues to remain extremely high.

Another interesting factor is that the average American’s FICO or credit score is the highest it’s ever been in history. Since scores are driven by debt, available credit and on-time payments, one could deduce that consumers are in an exceptionally good position to not only continue current trends, but even ramp spending up if more perceived risks (like trade, and impeachment) are minimized.

GDP Stable, Dollar Strong, Trade Still in Question

After a dip in the fourth quarter of 2019 and strong rebound in first quarter 2019, U.S. Gross Domestic Product has maintained a moderate pace of about 2% in the second and third quarters of the year. And while we still await fourth quarter GDP results, several other economic barometers showed signs of strengthening as the year came to a close — those boosts in productivity in manufacturing are likely to help bump GDP readings up a bit in fourth quarter with forward estimates likely to even out around 2%, unless the end of the trade war with China unleashes additional activity that hasn’t already been factored in.

Given the extremely accommodating and fast-acting action of the Fed in 2019, their language seems to suggest a low probability of this continued aggressive action. The CME Group fed rate futures suggest about a 50% chance that rates will remain at current levels by December 2020, with a 35% chance of another 0.25% cut and about a 15% chance of a more aggressive move. Economic indicators will dictate future action, but we do not see further reductions occurring during the first half unless a crisis ensues.

With much of the globe still mired in anemic growth, international trade volumes are likely to remain low, with a continued reduction in imports to the U.S. on top of moderating exports. Part of this is the growth of services over product sales. As many trade agreements remain unclear, business may look to source more from their home countries rather than from foreign suppliers. Despite interest rate cuts, the U.S. dollar Index is still about 10% higher than it was a year ago, making our exports more expensive to overseas buyers. The dollar is unlikely to reverse course unless other major economies show more economic strength, or the Fed eases significantly more. Neither of these possibilities seems very likely.

On trade, China needs to deal more than we do. Its massive population, slowing growth and lack of certain food resources make favorable trade deals imperative. China seems to be acquiescing to these realities and recently announced an import tariff cut on frozen pork items, pharmaceuticals and some tech components — a total of 859 types of products cut to lower levels, with some going to zero. Beijing promised to increase imports from the U.S. by $200 billion over the next 2 years, including the purchase of at least $40 billion in U.S. farm goods annually. And while we don’t know just how much China will participate in trade deal 1.0, the end of this tit-for-tat, 2-year trade war should bring a much-needed reprieve to global markets and confidence, and will certainly boost President Trump’s re-election bid probability.

We look forward to learning more about the next phase of our trade deal which should include protections for foreign entities in China, with a focus on intellectual property. The United States-Mexico-Canada Agreement (USMCA) should also stimulate modest economic growth in North America and is yet another “feather in the cap” for President Trump.

2020 Market Outlook Summary

Just as stated in our mid-year outlook, Westwood sees ongoing, stable growth in the economy, with a potential increase in the first half, followed by a likely slowdown going into U.S. elections. The upward global economic cycle could see a further boost from trade agreements and is likely to remain supported by extremely accommodative central banking tactics. Central banks will continue to fund their balance sheets to keep credit flowing, rates low and volatility under control. Stateside monetary policy remains extremely accommodative, but look for a reduction or pause in cuts for 2020. Market volatility may rise in first quarter 2020, both from a statistical and circumstantial perspective.

Federal Reserve Chair Jerome Powell added to his unusual “market support” commentary in 2019 by expressing a concern that inflation was under the Fed’s target and noted that he would like to see core Personal Consumption Expenditures Price Index (PCE) higher than where it’s been trending.

We are moderately concerned about the trend in corporate earnings growth, which has been continuously slowing, but believe that the improvement in economic data and positive trade developments will help spur consumer activity, corporate deals and CapEx spend.

Wage inflation continues to be modest and should remain tempered for the near future. Wage increases aren’t likely to translate into big jumps in the core PCE, but energy may be a contributor to a small bump in inflation early in 2020. That said, we expect PCE core inflation to remain subdued for the first half of the new year. And that lack of inflation right now is one key to keeping the central banks accommodative. Global banking rates are also on our radar as they can motivate U.S. Fed policy rates.

Outlook Positives

- Fed remains supportive of markets – As we’ve stated in our mid-year report, the Federal Reserve has played a key role in this expansion and is likely to remain accommodative for as long as it takes. There will likely be a slowdown in the pace of cuts and a less aggressive tone in the coming meeting, but actions will be commensurate with economic data. Chairman Powell stands at the ready to act and doesn’t seem concerned with the moderate inflationary boost we may experience. Global Central Banks will remain engaged and working to support this same theme.

- Inflation – Likely to increase moderately but remain below target rates. We may see a slight uptick as Chinese buying of American commodities comes alive and OPEC output cuts support crude prices. That said, we do not expect inflation, or inflation expectations, to rise considerably in the first half of 2020.

- Consumer remains strong – Consumer confidence continues to trend at highs, unemployment is low and wages are increasing modestly. The U.S. housing market has unlocked a tremendous amount of equity that could be accessed for additional spending. Conversely, housing prices are at record levels in much of the U.S., which could soak up dollars that might have been put to use elsewhere.

- Modest expectations – Equity markets have set the bar low for earnings growth; valuations are not extraordinarily high relative to historical levels and executives have done a good job, in general, in detailing risks to investors. This should limit the downside “surprise” factor.

- Sales and profits remain positive – Earnings and revenue growth are expected to remain positive for the early part of the year.

- Trade deal progressions – The Trump administration managed to solidify the USMCA and China Deal 1.0. These agreements should foster (in theory) reduced volatility, increased commerce and lower costs to the consumer.

Outlook Risks

- More work to do on trade – Even with a tentative agreement between the U.S. and China, we still need to see details and have both it and the USMCA ratified. There are also remaining trade disputes (metals, tech, auto imports) that will likely need to be addressed as investors begin to look for next steps with those and China by March or April. Negative outcomes could increase headline and actual risk, with the potential to slow capital investments from corporations. That said, the world seems to be gaining confidence that trade risks will continue to dissipate.

- Increased volatility – The last few months of 2019 were abnormally quiet. We expect volatility to rise as growth will be more selective in the coming months and election. Look for a continued gravitation to quality and value with less of an overall market “halo effect” for companies delivering mediocre results — investment selection will require added precision.

- Unexpected policy shifts – The current administration could abruptly shift its policies in a way that adversely affects commerce and/or trade. That said, we anticipate a highly favorable political and fiscal climate (at least on the surface) as the Trump administration vies for re-election.

- U.S. election dynamics – The upcoming presidential election could lead to great policy uncertainty and dramatic shifts in consumer sentiment, confidence and business investment. In the first half of the year, consumers and business owners will look to poll results and debates for clues that might lead to election outcomes. The ebb and flow of popular opinion, especially if leaning to an administration change, could have adverse effects.

- Central bank reactiveness – The U.S. central bank could begin to act less dovish given the appreciation in the housing and equity markets, as well as recent, positive trade agreements. Considering the negative impact the rising interest rate environment had at the tail end of 2018 and given the current inflation stance, it’s unlikely that a hawkish shift in Fed policy is coming. It’s also important to mention that the Fed has had to step in and create additional stimulative actions; including liquidity injections to control unintended increases in mortgage rates, for instance. There is a possibility that the effectiveness of its current actions will decrease in efficacy.